While I am an advocate for using travel credit cards for day to day purchases, there will be a point when you need cash. In many countries, credit cards are widely accepted but cash is still king and you must be prepared to have cash This is especially true when visiting less touristy locations and making purchases from local vendors. You have many options for getting cash while traveling – you can get foreign currency in advance from your local bank, exchange money at a currency exchange or the airport (please avoid this), or you can purchase traveler’s checks (apparently these are still used). However, those options are time-consuming and costly, and a travel debit card is a much better alternative.

I’ve tested most of the above options and I can confirm that getting a travel debit card is the most cost and time-friendly option. It has the added benefit of being the most secure option as well because you don’t have to carry a lot of cash at one time. Sure you have your regular debit card and can easily just use that to get cash at your destination, but what makes a travel debit card different are features like, no foreign transaction fees and not ATM fees This can save you so much money while traveling, and is also convenient when you need to get cash in your own city. Continue reading to learn what you should look for in a travel debit card, why I recommend the Charles Schwab debit card, and what are some alternatives for you to consider.

What to Look For in a Travel Debit Card

The Perfect Travel Debit Card

It’s ideal to get a travel debit card that saves you money not just in foreign transaction fees, but with all the fees involved with withdrawing money. The priority should be finding a card with no foreign transaction fees when using your debit card, but a card with low fees can also be worthwhile. Next you want to make certain that there are no ATM fees being charged by your bank for using your card at a out-of-network ATM. Since you will likely be using this card outside of your home country, it’s best to get a Visa or MasterCard card because they are the most widely accepted card networks. One feature that separates the best travel debit cards from the rest of the pack is the luxury of being refunded all of the ATM fees that are charged by the ATM you used for withdrawal.

Lastly, as with any other prospective debit card, you want to make sure that your’e not being charged fees for the sake of keeping money in your account. While most banks allow you to avoid monthly account maintenance fees by keeping X amount in your account or conducting X amount of transactions monthly, it’s best to find an account that requires none of that. Some other arbitrary requirement, like a brokerage account or membership, is far more reasonable in comparison.

Import Note: I would be irresponsible if I don’t mention this one thing – make certain you decline the ATM/bank conversion whenever you withdraw money! There will be a screen that pops up, prior to the confirmation of your withdrawal, that asks you if you want to accept the bank’s conversion by using their conversion with your bank instead of the local currency. Always decline the conversion if you’re using a good travel debit card, and seriously weigh your options if your debit card has a foreign transaction fee. If you are at all confused while withdrawing money, just decline and start over – some of these ATMS do make it hard to understand what you are and are not agreeing to.

Highly Recommended: Charles Schwab Debit Card

Pros

Cons

*There may be a way to avoid the United States Resident requirement, but I’m certain that will require paid brokerage services of some kind.

As you can see, the Schwab debit card exceeds all of the requirements that you’re looking for in a travel debit card. There’s a favorable conversion rate paired with no foreign transaction fees so you can happily decline the conversion ripoff that foreign ATMs like to offer to you. If that’s not enough, Schwab does not charge you any fees for using ATMs and they refund you once a month (see below) for any ATM fees that you incur from other establishments!

No debit card is perfect, not even Schwab but they do offer the best bang for no bucks! You’re probably wondering what’s the catch…and don’t you worry there is one. The Schwab debit card is almost like a freemium debit card option, but instead of spamming you with ads like games do or locking the best features behind a paywall, they simply require you to open a Charles Schwab brokerage account, which is also free.

Obviously, being a brokerage, Schwab is offering such a great checking account and debit card in hopes that you will utilize their paid brokerage services. For some, like myself, you may already have a Schwab brokerage account from company stock units or for personal trading. Another downside, for some, is that Schwab’s checking account is online only so there’s no Charles Schwab branch location that you can go to go in person to make cash deposits – if you already have an online bank account, you’d be unfazed. The other major downside, is that this product is only available to U.S. residents. Most of the other cons are fairly small in comparison, but a notable one is that the app is horrible. But the pros far outweigh the cons for me and I would recommend this card every time.

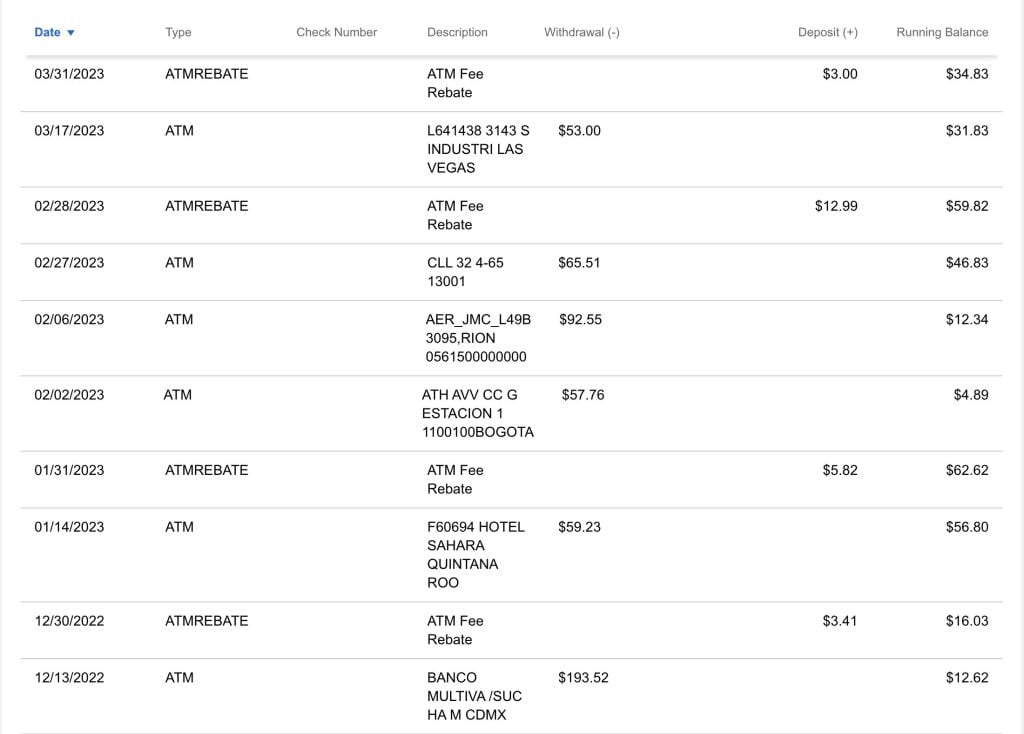

As you can see on the screenshot to the left, I’ve been withdrawing money on a regular basis in several different countries, and getting refunded regularly for the fees that I’ve been incurring. This has been an excellent solution for me as I can easily use Zelle to send money from my one of my other bank accounts to Charles Schwab checking account – I’ve even done this while I was at the ATM! Once I have the money in my account, I can just proceed with the withdrawal and go about my day. I don’t, generally, keep more than $50 in my Charles Schwab bank account so I’m not at all concerned about anyone getting access to my money.

Good Alternatives